Fondul Proprietatea is “the cheapest fund in the world”, said Mark Mobius, executive chairman of Templeton Emerging Markets Group, in a press conference in Bucharest, after the GSM on October 29. Poor liquidity keeps the assets of Fondul Proprietatea – 90% of them in the energy sector – dearly undervaluated. The situation forces the fund managers from Templeton Emerging Markets Group (TEMG) into unusual increased dynamics for bringing value to the shareholders. A strategy which gained Franklin Templeton a new extension of its mandate as manager of Romanian property restitution fund Fondul Proprietatea for two more years starting April 1, 2016.

Energy stocks make 15 of the top 20 portfolio holdings of Fondul Proprietatea. However, only three of these companies are listed – OMV Petrom, Romgaz and Nuclearelectrica. One of the most important is in insolvency – Hidroelectrica. 10 others are subject of bitter, if not totally stalled negociations: the fund would preffer to sell its minority stakes, while the majority holders are not interested in buying. “We are captive shareholders”, summarized the situation Greg Konieczny, executive vice president TEMG and portfolio manager for Fondul Proprietatea.

Captive Shareholders

Proposals are still being sent to and fro, without any positive expectation fom any side. In total, there are 8 electricity and gas distribution companies where the controlling stakes are held by foreign energy companies, including Germany’s E.ON, Italy’s Enel and Gaz de France / Engie. “Having unlisted companies in the portfolio usually results in a higher discount to NAV [Net Asset Value], and we want to make the portfolio more liquid,” Greg Konieczny explained in May 2015, for British financial media. “When they list we could stay as a shareholder, exit completely or reduce the holding,” he also said. For the moment, the fund has ongoing discussions with Enel, while it challenged the business strategy consultancy agreements between E.ON Distribuție Romania and E.ON Energie Romania, on one side, and their majority shareholder E.ON Romania SRL, on the other. Fondul Proprietatea is determined to start litigations against the companies’ board members and managers of these companies for approving, concluding and performing agreements, with an estimated cumulated value of damages of RON 34.4 mil, in 2014. On the GDF Suez Energy Romania situation no details are available from the fund.

A possible exit from the current stalemate could come from the Romanian Government if it will succeed on forcing the listing of these privatized utility companies, against the common practice that states that no international company keeps its subsidiaries listed.

But Fondul Proprietatea and the Romanian state clash on another group of 4 electricity companies, subsidiaries of the recently listed Electrica. The fund holds 22% of each the subsidiaries – which are valued at almost EUR 189 million in its portfolio, while Electrica is 49% controlled by the state. In Spring, Fondul Proprietatea withdrew an offer it made to Electrica to sell the four subsidiaries for a price closer to EUR 100 million, as it was circulated, although not confirmed, in the Romanian media. Fondul Proprietatea is now ready to restart negotiations, as some of Electrica’s minority shareholders obtained in a General Shareholders Meeting approval of the mandate of the Board of Electrica to negotiate and close the transaction with the fund.

Balancing the future with the present

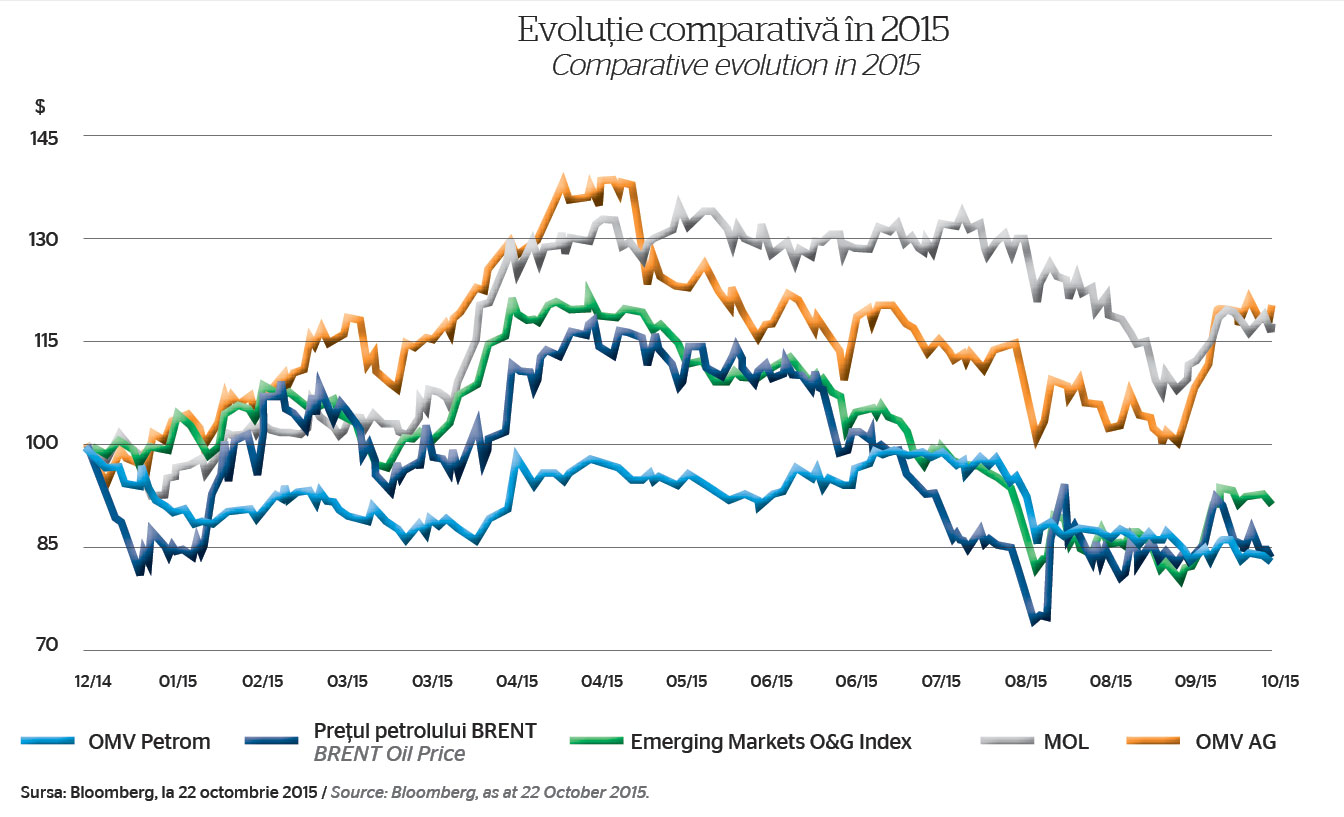

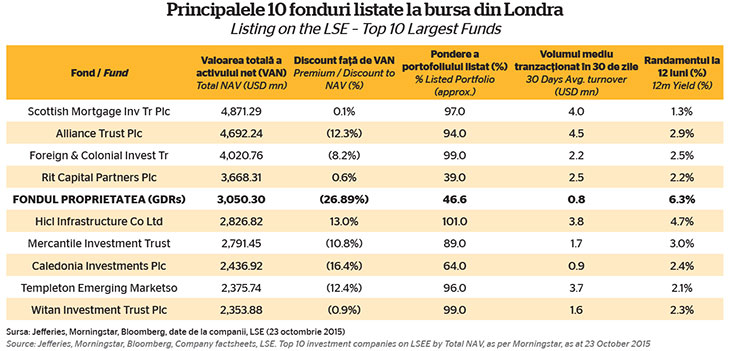

Mainly based on these energy companies, Fondul Proprietatea is by far the most profitable among the largest 10 funds on the London Stock Exchange; it recorded a 12 months yield of over 6%, while most of the other nine stay well under 3%. Still, the poor liquidity of the shares is what prevents the Romanian O&G leading companies to perform near their industry peers on the stock markets. OMV Petrom shares closely followed the decline in Brent Oil prices in 2015, but they were strikingly outpaced by the recent months rebound of Emerging Markets Oil & Gas Index, and shares of MOL and OMV AG.

The Romgaz shares fared slightly better, though they are now almost 15% lower than 12 months ago. In October, Fondul Proprietatea sold through an accelerated private placement 4.15% of the stakes in Romgaz, for a total of RON 456 million (EUR 103.1 million), with a discount of 6.4% to last closing price. Upon completion of the transaction, the fund remaind with 22.54 million Romgaz shares, representing 5.85% of the capital.

Greg Konieczny defended the selling with just another powerful sentence: “We are not desperate sellers!” And the fund got the shareholders’ support to go on with this policy of selling its most liquid holdings even at discounted prices. Fondul Proprietatea is “the cheapest fund in the world”, explained Mark Mobius. The most attractive investment for the fund are the buy-back programs of shares and GDRs. All is aimed at maximizing cash returns to shareholders. On the long term, selling Romgaz shares is one form of stimulating the local stock market, with beneficial effects to the fund. After all, the operation attracted numerous investors from CEE, Scandinavia, US and UK, and also proved that there is a strong local apettite for Romgaz shares – 45% of the total demand came from Romania, both institutional and retail.

The Land of Great Opportunities

Last couple of years, the fund performance was affected by difficult market conditions, with significant declines in prices for oil, gas, and electricity, and also heavy insecurity due to events in Greece and Ukraine. Numerous changes in regulatory framework by the FSA also affected Fondul Proprietatea. A deluge of events (Hidroelectrica re-entering the insolvency procedure, introduction of the infrastructure tax of 1.5%, reduction of the regulated rate of return of the electricity distribution companies from 8.5% to 7.7% of the Regulated Asset Base) and non-events (delays in the IPO calendar of the state own companies, delays in the gas liberalization for households, delays in publication of the new law on taxation of the oil and gas sector, delays in implementing the corporate governance code) influenced the energy market and shifted into the fund performance.

The corporate governance code implementation will continue to be a cornerstone for the proper functioning of the companies under the Romanian state authority, consider the managers of Fondul Proprietatea. The proposed updates for the law 109/2011 are far from being satisfactory whilst the minority shareholders rights are still not strong enough, and the Parliament and ministries do still have discretionary powers.

Answering a question from energynomics.ro on the dispute around Electrica’s management, Greg Konieczny remarked that the numbers the company communicated are good and there are positive changes at the subsidiaries level. “I don’t know why the Government goes into this procedure of changing the Board of Electrica’s”, Greg Konieczny added. The TEMG’s representative expressed his believe that Hidroelectrica’s listing will more than likely happen in 2016, after the energy producer will exit insolvency. Not the same prospect for CE Oltenia, where the proceedings were de facto suspended.

“Assets here [in Romania] will become more and more valuable”, considers Mark Mobius. However, TEMG’s officials chose to ignore, for the public, an additional explanation for the huge discount to NAV: the investors’ concerns about the exposure of the fund’s assets to political influence. The 34 unlisted companies inthe portfolio are huge unknowns even for the managers and the most difficult challenge ahead of them. The same as it was in 2011; it is just that back then the average annual discount to NAV neared 56%, and in 2015 this indicator will most probably descend under 30%.

————————————-

The full version of this article can be read in printed edition of energynomics.ro Magazine, issued on December 2015.

In order to receive the next issue (March 2016) of energynomics.ro Magazine for free, we encourage you to write us at office@energynomics.ro to include you in our distribution list.